SEMA News - July 2009

RESEARCH

By Jim Spoonhower

Providing Looks, Features and Creature Comforts to Mainstream Consumers and Automotive Enthusiasts Alike

| |

| In 2008, retail sales of restyling specialty-equipment products reached $3.958 billion. Restyling product sales currently represent about 12.4% of the total automotive specialty-equipment market. |

|

It wasn’t all that long ago that the OEMs were trumpeting the concept of mass customization. The idea sounds great, particularly to consumers. After all, under mass customization, all vehicle buyers could get exactly what they want because essentially each vehicle would be built to order.

Why all the emphasis on mass customization? Because today’s markets are changing faster than ever, and consumers are becoming more demanding than ever. Customized products are being offered everywhere you look: design your own tennis shoes with Nike; word your own M&Ms; create your own computers; and personalize your cell phone. As consumers become increasingly accustomed to having the products they buy tailored specifically to them, the demand for customized vehicles will grow.

Mass customization was viewed as a solution to address new market realities while still enabling the OEMs to capture mass-production efficiency advantages. Considering the production-cost issues the car companies have, they decided to offer increasing numbers of models and options to satisfy consumer demands.

Traditionally, customization and low cost have been mutually exclusive—mass production provided a low cost, but at the expense of uniformity. Customization was the product of passionate designers and craftsmen. Its expense generally made it the preserve of enthusiasts. Today, mainstream consumers are learning about the possibilities and asking for their vehicles to be exactly what they want.

All of this came about in an attempt to give the consumers what they want. And to think, the performance parts and accessories industry has been built and grown on that very concept.

We know this segment of the industry as restyling. Restylers don’t necessarily limit their attention to a particular vehicle type or a specific OEM, but rather concentrate on personalizing the vehicle to the customer’s wants and expectations. Some restylers work mostly with new-vehicle dealers. Others have built an extensive loyal customer base in their target market. Whether it’s new or used vehicles that are being updated and dressed up, the result is always the same—consumers get a vehicle that is unique to them.

As a result, restyling has grown to be a large piece of the performance parts and accessories industry. In 2008, retail sales of restyling specialty-equipment products reached $3.958 billion. Restyling product sales currently represent about 12.4% of the total automotive specialty-equipment market.

When you look at the industry from the consumer’s perspective, you find that they have a particular result in mind when modifying their vehicles. The off-roader has certain features and capabilities in mind that modifications will provide, the compact-performance tuner has a different set of goals and so it goes with each niche market.

For what we call restyling, the intent of the consumer is to personalize the vehicle in general terms that would not result in it fitting into one of our other defined niche markets.

| |

| As consumers become increasingly accustomed to having the products they buy tailored specifically to them, the demand for customized vehicles will grow. |

Market Size

To be sure everyone is on the same page, when we refer to the restyling market, we’re including all the products used to modify the exterior and/or interior of vehicles. That covers a wide range of automotive specialty-equipment products, from sunroofs to ground effects and from grille guards to drop-center bumpers.

All of the products found in this market are functional, though, the principal reason for their purchase may be more aesthetic. After all, some consumers purchase these products just because of the vehicle’s look after installation.

Most restyling products are designed to work with or complement the existing lines of the production vehicle. In fact, many concepts and accessories created in the restyling market have become part of production vehicle designs.

The restyling market did not show positive growth in 2008. Much of the cause can be attributed to the amount of business restylers do with new-car dealers and the huge drop in new-car sales last year. Considering that new-vehicle sales dropped from 16.5 million units in 2007 to 13.5 million in 2008, a decrease of 18%, the decrease in restyling sales of 6.34% is almost positive.

As we look at our industry, we typically segment products into one of three categories: accessories and appearance products; performance products; and wheels, tires and suspension products. Many of the vehicle modifications in the restyling market involve automotive accessories. In fact, accessories represent more than 66% of the products sold in the market for 2008. Of the defined niche markets that SEMA studies, accessories has the highest market share in the restyling market.

|

| |

| In 2008, retail sales of restyling specialty-equipment products reached $3.958 billion. Restyling product sales currently represent about 12.4% of the total automotive specialty-equipment market. | ||

SEMA Index

In April, the SEMA Performance Parts and Accessories Demand Index (PADI) decreased, going from 30 in March to 26. That translates to approximately 7% of adult American drivers indicating that they had plans to purchase performance parts and accessories sometime within the next three months.

About 4% of consumers said that they were likely to purchase wheels, tires and suspension components; 3% said that they were likely to purchase racing and performance products; and 4% said that they were likely to purchase specialty accessories and appearance products.

On average during the months of February, March and April, fullsize cars (22%) were the most common target vehicles for enhancement or modification, followed by midsize cars (20%), pickups (13%) and compact cars (11%).

When consumers were asked what form their vehicle would take after customization, the most common answer in April was general personalization or restyling (46%), followed by street performance (15%) and off-road (10%).

SEMA began developing the PADI in January 2007. The purpose of PADI is to track anticipated demand among Americans for performance parts and accessories, such as specialty appearance, racing and performance as well as wheels, tires and suspension products.

The PADI is a weighted composite index—set to an initial value of 100 based on demand levels between January 2007 and March 2007. During those months, between 25%–30% of consumers reported plans to purchase performance parts and/or accessories during the next 90 days.

The index and three subindices (for each product segment) are based on the responses to the following questions:

How likely are you to purchase specialty accessories and appearance products, such as interior trim, restyling products, graphics, a sunroof, etc., for your vehicle in the next three months? Would you say very likely, somewhat likely, not very likely or not at all likely?

How likely are you to purchase racing and performance products, such as internal engine parts, drivetrain, exhaust system, fuel system and ignition components designed to improve performance through increased durability, capability or dependability for your vehicle in the next three months? Would you say very likely, somewhat likely, not very likely or not at all likely?

How likely are you to purchase wheels, tires and suspension components, such as specialty shocks, struts, lowering packages, lift kits, custom wheels, performance tires or performance brakes (not including regular brake changes) for your vehicle in the next three months? Would you say very likely, somewhat likely not very likely or not at all likely?

The index is based on a monthly random digit-dial telephone survey to collect the survey data. Typically, it is based on around 1,000 nationwide interviews with adult American drivers. The margin of error is +/- 3.3%.

Although the PADI is not a precise measure of absolute future purchasing activity, it is nonetheless a tool for understanding and predicting industry sales. There are two ways of interpreting the PADI. First is its direction—whether the index is rising or falling. Second is that the values themselves provide a guide as to the degree of change in consumer expectations for purchasing industry products.

So what has all this got to do with the restyling market? Notice that 46% of consumers queried in April were thinking about restyling projects for their vehicles during the following 90 days. When you consider that the data collection is not limited to automotive enthusiasts, it would be easy to draw the conclusion that mainstream consumers are entering our market through the restyling niche. Whether perfecting the new vehicle they just purchased or bringing the existing one up-to-date, increasing numbers of mainstream consumers are finding our industry.

One need only look at how similar many of the vehicles on today’s roads appear to understand why the restyling market has grown so large. After all, these products make each vehicle as individualistic as its owner. They provide the looks, features and creature comforts that just don’t come with production vehicles to mainstream consumers and automotive enthusiasts alike.

A Bright Spot in a Challenging Economy

If you have been paying any attention to the news, you know that GM and Chrysler are eliminating new-vehicle dealer franchises in the United States. We stand to lose nearly 2,000 new-vehicle dealers over the next few months.

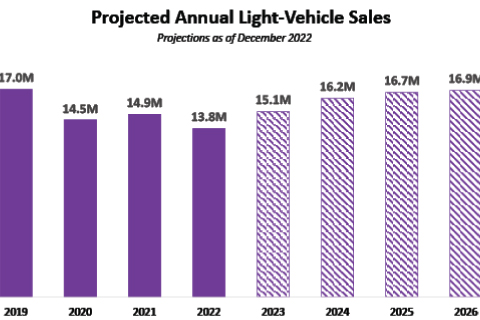

The auto industry and the automotive performance parts and accessories industry have become accustomed to new-vehicle sales in the 15–16 million unit range. After all, annual new light-vehicle sales have been above 15 million units every year since 1996—until 2008 when they dropped to 13.5 million.

“AutoPacific forecasts a gradual industry recovery over the next five years as the economy recovers, to just under 15 million units by 2014,” reports Carol Runkle, manager of AutoPacific sales forecast service.

A number of SEMA-member companies have grown to depend on new-vehicle sales to drive their business. So what are they to do? A retailer in Maryland has a workable solution. Mark Miller of Westminster Speed & Sound started noticing that his customers were parking their crew-cab diesel pickups and buying used vehicles that got better gas mileage. Gas prices were making their preferred vehicle just too expensive to drive.

Miller’s customers were soon back in his store looking for ways to “spruce up” their new used car. They wanted some of the features they became accustomed to in their fully loaded trucks. The final straw that connected the dots for Westminster Speed & Sound was the realization that the car manufacturers were also offering low-cost new vehicles without all the options consumers have grown used to.

So now, this retailer is building a new business around “sprucing up” used vehicles and customizing new low-cost basic models. His customers are now asking for custom wheels to replace the “steelies” that came on the car. They are also looking for rear spoilers, exhaust systems, window tint and technology that used to be standard equipment.

To help with his marketing, Miller even bought a “stripper” model used car to fix up and show his customers what could be done. He chose a car that gets good mileage and is adaptable enough to be easily customized—a 2008 Chevy Cobalt two-door LS coupe. This car looks just like the newer ones on the car lots, but costs a lot less.

Some of the things that this car will get are: power windows; door locks with keyless entry; and remote start. The sound system will get a makeover that will include iPod, Bluetooth and HD radio integration into the original radio plus upgraded speakers, an amplifier and a subwoofer. Westminster Speed & Sound will install an air intake system and exhaust system for more power and improved fuel mileage. There will be new struts, lowering springs and swaybars to improve the handling.

The exterior will get a rear spoiler, some window tint, a new grille, driving lights, backup sensors, a backup camera and a nav system. Miller’s crew will add dampening material to quiet the road noise. This car will become a rolling showcase for all the things a consumer wants, but doesn’t have in their less expensive vehicle.

Everything that goes into the demo car is something everyday people can afford and enjoy. Miller even plans to call on some of his local car dealers and show them the demo car as a way of building more business.

Here is a retailer who connected the dots of what he was seeing happening in his marketplace and adapted his business model. Truly a bright spot in a challenging economy.

—Jim Spoonhower