SEMA News—September 2019

BUSINESS

The “2019 SEMA Market Report”

Automotive Specialty-Equipment Sales Climb to a New High of $44.6 Billion

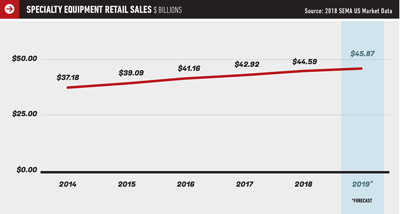

Specialty-equipment parts sales hit a new high in 2018 of $44.6 billion. Sales are projected to reach nearly $46 billion in 2019. |

The automotive specialty-equipment market kept humming along to the tune of $44.6 billion in total parts sales in 2018—a 4% increase over 2017, according to the just-released “2019 SEMA Market Report.” Rumors continue to circulate that young people have disengaged from the automotive aftermarket hobby, but that couldn’t be further from the truth. Young customizers spent more than $7 billion on parts.

The economy started to experience some volatility last year, and more of the same is expected into 2019. As of now, however, consumer sentiment is still strong, and people are still spending. Slower growth is forecasted through 2019, with projected retail sales to hit a new high of nearly

$46 billion.

“There is still a lot of uncertainty,” noted Kyle Cheng, SEMA market research manager. “Our market tends to be discretionary, so disruptions such as trade wars could dampen our growth projections, but the industry is still positive and market signs are still good as of now.”

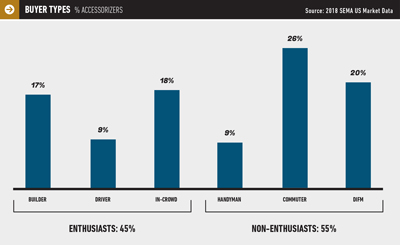

Non-enthusiasts make up 55% of the total specialty-equipment market. |

A Non-Enthusiast Majority

It’s important to note that enthusiasts are not the majority of accessorizors; they make up 45% of consumers. A slight majority are non-enthusiasts who purchase less-glamorous parts such as wheels and tires, which SEMA Market Research Director Gavin Knapp refers to as the “gateway drug.” Consumers often start there because those products make an obvious visual difference and sometimes lead to other modifications as consumers catch the bug.

“Or maybe they’ll do wheels and tires and nothing else,” Cheng said. “They want other people to do the work for them. However, enthusiasts tend to spend the most money on parts and do the more extensive modifications.”

Some people are motivated by appearance, so they may be into external accessorization, while others are into traditional under-the-hood performance.

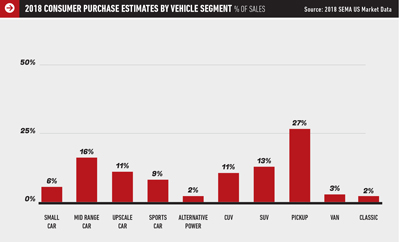

Pickups Remain Industry’s Driver

The automotive specialty-equipment market is splintered into several different vehicle segments, with pickups once again making up the largest share at 27%. Product growth varies by segment, but off-road tires, exterior utility items and suspension systems are the most profitable with pickups.

“Pickups are the perfect vehicle for us,” Knapp said. “You can do anything from lifting to appearance and functional stuff. It will be interesting to see whether consumers will behave like car buyers or truck buyers as OEMs create fewer sedans and move their resources toward CUVs and SUVs, and whether they will look for performance parts or accessorize for fun and utility.”

Ford has announced plans to stop production of many of its passenger cars, but with the average lifespan of a vehicle at about 10 years, it will take that long for the change to trickle into the market. Due to high gas prices and a shift toward smaller engines, consumers want power, but they want fuel efficiency, too, which is partially why CUVs are more popular.

“People like power, but they don’t want to pay for it,” Cheng said. “You don’t find a lot of V8s now; instead, you find a lot of turbocharged V6s.”

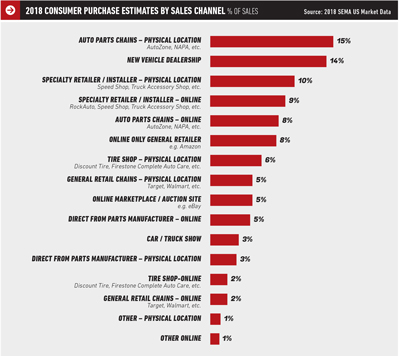

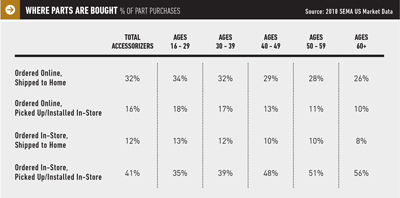

Nearly 60% of specialty-equipment parts are purchased at physical locations vs. 40% purchased online. |

The Emergence of ADAS

Although the industry is witnessing an extended growth period across the board since the last recession, one area that has experienced the slowest growth is the mobile-electronics segment, which has remained stagnant during the past few years at just over $1 billion. However, advanced driver assistance systems (ADAS) are relatively new to the market over the past couple years and continue to grow as more products become available.

“ADAS is a new market for us to track, so there’s not a lot of history to determine trends,” Knapp said. “People are still trying to figure out where the opportunities are. With ADAS, the products that are available to consumers as retrofit are simplistic, such as backup cameras. As retrofit, we don’t have the same options as the OEMs.”

Pickups comprise 27% of the vehicle market. |

Online vs. Retail Sales

While the digital marketplace continues to grow, brick-and-mortar sales (59%) still outpace online sales (41%). This year’s report contains information across the different parts types about how consumers order and pick up.

“You can go into a store and have parts sent to you or order online and have them sent to you, but we’re seeing a good chunk of people who order online and go pick the parts up,” Knapp said. “It varies based on product category, and shipping has something to do with that. There are also differences in products that you would want immediately. You could buy oil online and wait for it, but if you’re changing your oil, you’re probably going to want to do it now, so you would go into the store and pick it up.”

Sales-channel preferences depend on how easy it is to do the work yourself and the degree of difficulty in finding products. For instance, parts for classic cars and engine upgrades tend to be easier to find online.

Age and ability or comfort level within the hobby are also factors in buying behavior. Older consumers are more used to going to the store for purchases, while those with the most ability tend to purchase more online because they don’t need the reassurance of talking to a salesperson and are less likely to need someone to install parts for them. Hardcore consumers can make up their owns minds, do their research online and have parts shipped

to them.

About 41% of total accessorizors ordered parts in-store and picked them up themselves. |

Youth Engagement

The SEMA market research team recently completed the “SEMA Young Accessorizors Report”—a study on the buying behaviors of young people in the industry—and data from the “2019 SEMA Market Report” backs up what they found. The highest accessorization rate is among young consumers, and it slows as they get older.

“Younger people are the most important piece of our industry,” Knapp said. “About a third of our industry is under 30 years old. There is always the perception that young people don’t have any money; however, they have time and desire, so they will spend all the money they have on what they desire.”

Younger consumers are more likely to spend money on extensive and complicated procedures, such as under-the-hood modifications. For them, it’s more about showing off on social media.

“Part of that is ‘Look what I got, look what I can do,’ and they post everything on social media,” Knapp said. “The big takeaway is that we don’t find that young people are deserting our industry. People say that this generation is all about personalization. Why think that someone is going to personalize their phone, which you’re not going to see because it’s in their pocket, but they’re not going to personalize the car that they drive on the road

every day?”

About 79% of consumers who bought chemicals were do-it-yourselfers, while 67% of those who purchased wheels and tires had them professionally installed. |

Reaction to Gas Prices

Although gas prices have increased recently, it is not affecting consumer behavior much. Consumers are still projected to purchase larger cars with supercharged and turbocharged engines; however, high gas prices over an extended period might push manufacturers to build smaller engines that are both more powerful and more fuel efficient.

“As we see these little spikes and fluctuations, there doesn’t seem to be a big consumer reaction to it or that it’s going to be an ongoing problem,” Knapp said. “There is a trend toward smaller engines with forced induction, not necessarily in response to higher gas prices but in response to higher expectations of

fuel economy.”

The Bottom Line

| “2019 SEMA Market Report” Fast Facts |

|

Despite an unpredictable economy, the automotive specialty-equipment industry is still going strong, according to Cheng, and most experts don’t foresee a recession for at least another year. People are still cautiously optimistic. Just last May, the index for consumer sentiment topped 100 for only the fifth time since 2010, and the job market is at full employment.

“We are in the longest growth period since the last recession,” Cheng said. “There’s a lot of uncertainty and uncertainty causes panic, but panic doesn’t always lead to a recession. No one knows when the next one will happen; it won’t be as bad as in 2008 and 2009, but recessions are a natural part of our economic growth.”

Although the economy is still robust, Cheng cautions that one bad policy—for instance, ongoing trade wars—could derail the industry because it is so reliant on the global supply chain that any disruption could be detrimental. Tariffs are not helping either because fear has actually driven the price of steel up.

Looking ahead, Knapp projects continued but slowed growth for the industry, partially due to a slowed growth rate in new-vehicle sales.

“OEMs are still selling vehicles at historic levels; they’re just not growing those levels year after year,” Knapp said. “That impacts us because people start to accessorize as soon as they buy a new vehicle. With tariffs, the big question will be if the input prices of steel and aluminum push prices of our industry’s parts up. Will manufacturers internalize higher costs or push them directly out to the consumer?”

The “2019 SEMA Market Report” is free and a benefit of SEMA membership. Along with a host of other free industry reports, it can be found at www.sema.org/market-research. The SEMA market research team is available to help the industry directly. If you have any specific questions, contact SEMA Market Research Manager Matt Kennedy at mattk@sema.org or 909-978-6730.

| Where Does the Data Come From? |

For nearly 30 years, SEMA has produced its annual market report with the goal of helping membership understand the size and shape of the automotive specialty-equipment market, look for trends over time, and hone in on particular market subsectors. The data comes from a variety of sources. The main market-sizing estimates that comprise the bulk of the study are based on a large-scale consumer survey that is sent to a representative population of drivers across the United States. SEMA surveys more than 20,000 people to find out what kinds of vehicles they own, what they do with them, whether they buy specialty parts and accessories, where they buy them, how much they pay, etc. SEMA market research dives deep into forecasting in terms of expected future trends based on the “SEMA Future Trends Report.” The market research team also produces a monthly “SEMA Industry Indicators report,” which provides government information about how the economy is doing. A snapshot of the SEMA Show’s attendance and what sections are hot helps provide the industry’s pulse. Finally, SEMA highlights data from industry professionals about what they think about the state of the industry and whether they feel optimistic about the future. |