New SEMA Research to Guide Your Business Strategies

Advanced Driver Assistance Systems (ADAS) and Connected Vehicle Technologies (CVT) are poised for a disruptive transformation of the aftermarket. Now is the ideal time to assess your readiness for this revolution, and the latest SEMA research can help you seize the rapidly emerging business opportunities. |

SEMA research indicates that the U.S. aftermarket for advanced driver assistance systems (ADAS) and connected vehicle technologies (CVT) can be expected to grow into a $1.5 billion industry within the next five years, even though the emerging segment is still in its infancy. The impact of these new systems can’t be overstated. Hard as it may be to imagine, they will eventually affect virtually everything from wheel and tire modifications and vehicle electronics tweaks to the addition of custom bumpers, running boards, grilles and other hard parts. With so much at stake in these rapid-breakthrough technologies, SEMA has made identifying ADAS/CVT opportunities for association members a key priority.

According to the recently released “SEMA Advanced Vehicle Technology Report,” the current supplier landscape for these technologies is limited, spelling plenty of growth potential for new participants ready to enter the marketplace and stake out a strong presence in multiple product categories. In the meantime, channel and service providers must start now to acquire proper education, equipment and skilled personnel if they are to successfully adapt to this changing market and truly thrive.

While slow in the early adoption of ADAS/CVT products, American consumers are now not only warming to but also increasingly embracing them. As they become more and more accustomed to the added safety and conveniences offered by OEM ADAS/CVT packages in their new-model cars, drivers are expected to eagerly seek out similar supplemental products for all of their vehicles. The reason is obvious: The National Safety Council recently estimated that 20% of all motor-vehicle-related injuries can be tied to distracted driving. ADAS/CVT products can dramatically cut such risks. Add to that the substantially reduced risks of backover- and blind-spot-related accidents, and it’s easy to see why the more consumers learn about these technologies, the more they demand them.

The following are highlights of key overall findings from the “SEMA Advanced Vehicle Technology Report,” available for download at www.sema.org/avt-opportunities. Upcoming issues of SEMA News will continue to break down report specifics, topic by topic.

Key ADAS Aftermarket Systems (total million dollars upfit) |

The ADAS/CVT market had an estimated worth of $977 million in 2016 and is expected to reach $1.5 billion by 2021—a 9.1% annual compound growth rate. Source: Market Feedback, Ducker Analysis and CAR |

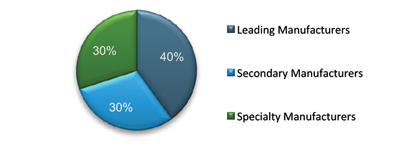

Market Share by Manufacturer Segmentation (by total revenue) |

|

Key ADAS Aftermarket Systems (total million units upfit) |

|

| ADAS Channel Evolution |

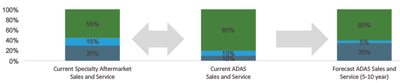

Although independent repair and specialty businesses currently take the lion’s share of ADAS sales and servicing, parts chains will gain a significant footing by 2022. Source: Market Feedback and Ducker Analysis |

New Opportunities

Based on its research, SEMA encourages its manufacturing and installing members to explore the opportunities presented by the fast-growing, high-margin ADAS/CVT markets. In making its “SEMA Advanced Vehicle Technology Report” available, the association hopes to help guide product and service planning and entry strategies for this emerging market. The SEMA analysis can help members understand the current market and its forecasted growth potential.

Amid this growth and rapid adoption of ADAS/CVT technologies, the specialty-equipment market will experience an unprecedented disruptive trend. These new systems are becoming increasingly common across OEM platforms, with consumers already weighing them in their buying decisions. Driver-assist technologies may currently represent only a relatively small share of the motor-vehicle aftermarket, but there can be little doubt that they are poised for rapid gains. Consider that electronic content in new vehicles is now greater than 40%. With current gross margins for these technologies between 40%–60% and rising, there will be increasing interest to replace, retrofit and modify the vehicle electronics systems on all cars.

Charting ADAS Strategies

In forming a market game plan, aftermarket businesses will want to fully understand not just the advanced technologies but also the timelines and channels of their rollouts.

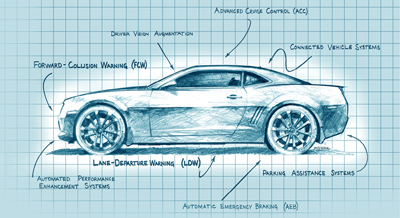

- Systems: Passive systems such as forward-collision, lane-departure and blind-spot warning, among others, will likely grow first and fastest. More complex active systems such as adaptive cruise control and automated braking may offer greater revenue potential, but they carry legislative and liability concerns, making them less attractive for the specialty-equipment industry.

- Adoption: Aftermarket suppliers will wish to carefully monitor OEM adoption rates as leading indicators of market acceptance. Today’s OEM penetration is already estimated at $7–$8 billion. Meanwhile, future legislation may determine access to OEM systems data, which will directly affect the aftermarket’s ability to offer OEM-level calibrated products.

- Channels: There will be many ways to engage ADAS/CVT business opportunities, including through part and component manufacturing, distribution, installation, repair and service. For example, aftermarket ADAS products are currently sold mainly through independent vehicle customization, repair and specialty-equipment shops. As the ADAS market expands, sales channel patterns will likely evolve toward traditional aftermarket models, with parts chains taking an increasing share.

For now, fleets account for the adoption of about 70% of current ADAS aftermarket products and will continue to drive sales in the near term. However, consumer awareness, needs and marketing will gain traction for ADAS products in passenger vehicles over the next two to three years.

Key Drivers and Technologies

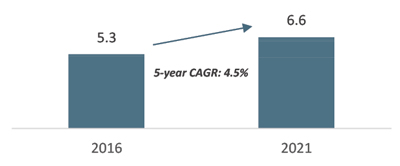

The ADAS aftermarket is on target to grow from 5.3 million total unit upfits in 2016 to 6.6 million units upfitted by 2021. Passive parking assist—a relatively simple technology—accounts for the majority of market growth. In addition, SEMA market research has identified blind-spot warning and passive forward-collision warning systems as high-growth categories. Key aftermarket growth drivers will include:

- The lower cost of aftermarket systems relative to OEM products, which are often included mainly in higher trim levels.

- The ability to utilize ADAS products on older vehicles, as well as late-model trim levels that do not offer the same options.

- The increased interest in safety systems on the part of end users.

- The ease of self-installation by customers for certain systems, such as passive parking assistance.

| Stay Informed! |

The tremendous potential ahead for the specialty-equipment industry is detailed in “SEMA Advanced Vehicle Technology Opportunities.” To download a copy of the report, go to Visit the SEMA Garage Vehicle Technology webpage at www.semagarage.com/services/vehicletechnology for additional information about ADAS technologies and how they may impact your business. |

The Bottom Line

To sum up, the aftermarket for ADAS is being driven by a blend of consumer demand for safety systems, new product availability and the growing ability of installers to offer these innovative and increasingly vital products for older vehicles. In addition, the aftermarket is positioned to offer cost-effective alternatives for newer vehicles whose ADAS options may be deemed by consumers too costly or insufficiently robust.

With a presently limited supplier landscape, there are real opportunities for new entrants into the aftermarket. Moreover, SEMA-sponsored research finds that the financing community is already welcoming ADAS participants with strong, forward-looking valuations. This research further suggests that the marketplace will evolve organically, with participants innovating new and unique value propositions and/or migrating to ADAS from other vehicle and sensor-technology segments. In other words, now is the ideal time to evaluate your business readiness for the ADAS/CVT revolution and consider how you can tap into this new segment’s tremendous potential.